LIST OF TABLES

TABLE 01. GLOBAL ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 02. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR SOLUTION, BY REGION, 2022-2032 ($MILLION)

TABLE 03. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR SERVICES, BY REGION, 2022-2032 ($MILLION)

TABLE 04. GLOBAL ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 05. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR ON-PREMISE, BY REGION, 2022-2032 ($MILLION)

TABLE 06. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR CLOUD, BY REGION, 2022-2032 ($MILLION)

TABLE 07. GLOBAL ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 08. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR MACHINE LEARNING AND DEEP LEARNING, BY REGION, 2022-2032 ($MILLION)

TABLE 09. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR NATURAL LANGUAGE PROCESSING (NLP), BY REGION, 2022-2032 ($MILLION)

TABLE 10. GLOBAL ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 11. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR LEARNING PLATFORM AND VIRTUAL FACILITATORS , BY REGION, 2022-2032 ($MILLION)

TABLE 12. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR SMART CONTENT DELIVERY, BY REGION, 2022-2032 ($MILLION)

TABLE 13. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR FRAUD AND RISK MANAGEMENT, BY REGION, 2022-2032 ($MILLION)

TABLE 14. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR INTELLIGENT TUTORING SYSTEM (ITS), BY REGION, 2022-2032 ($MILLION)

TABLE 15. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

TABLE 16. GLOBAL ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 17. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR HIGHER EDUCATION, BY REGION, 2022-2032 ($MILLION)

TABLE 18. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR K-12 EDUCATION, BY REGION, 2022-2032 ($MILLION)

TABLE 19. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR CORPORATE TRAINING AND LEARNING, BY REGION, 2022-2032 ($MILLION)

TABLE 20. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

TABLE 21. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY REGION, 2022-2032 ($MILLION)

TABLE 22. NORTH AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 23. NORTH AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 24. NORTH AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 25. NORTH AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 26. NORTH AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 27. NORTH AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COUNTRY, 2022-2032 ($MILLION)

TABLE 28. U.S. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 29. U.S. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 30. U.S. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 31. U.S. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 32. U.S. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 33. CANADA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 34. CANADA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 35. CANADA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 36. CANADA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 37. CANADA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 38. EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 39. EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 40. EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 41. EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 42. EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 43. EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COUNTRY, 2022-2032 ($MILLION)

TABLE 44. UK ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 45. UK ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 46. UK ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 47. UK ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 48. UK ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 49. GERMANY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 50. GERMANY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 51. GERMANY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 52. GERMANY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 53. GERMANY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 54. FRANCE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 55. FRANCE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 56. FRANCE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 57. FRANCE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 58. FRANCE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 59. ITALY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 60. ITALY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 61. ITALY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 62. ITALY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 63. ITALY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 64. SPAIN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 65. SPAIN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 66. SPAIN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 67. SPAIN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 68. SPAIN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 69. REST OF EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 70. REST OF EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 71. REST OF EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 72. REST OF EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 73. REST OF EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 74. ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 75. ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 76. ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 77. ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 78. ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 79. ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COUNTRY, 2022-2032 ($MILLION)

TABLE 80. CHINA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 81. CHINA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 82. CHINA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 83. CHINA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 84. CHINA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 85. JAPAN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 86. JAPAN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 87. JAPAN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 88. JAPAN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 89. JAPAN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 90. INDIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 91. INDIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 92. INDIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 93. INDIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 94. INDIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 95. AUSTRALIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 96. AUSTRALIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 97. AUSTRALIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 98. AUSTRALIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 99. AUSTRALIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 100. SOUTH KOREA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 101. SOUTH KOREA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 102. SOUTH KOREA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 103. SOUTH KOREA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 104. SOUTH KOREA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 105. REST OF ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 106. REST OF ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 107. REST OF ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 108. REST OF ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 109. REST OF ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 110. LAMEA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 111. LAMEA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 112. LAMEA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 113. LAMEA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 114. LAMEA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 115. LAMEA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COUNTRY, 2022-2032 ($MILLION)

TABLE 116. LATIN AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 117. LATIN AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 118. LATIN AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 119. LATIN AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 120. LATIN AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 121. MIDDLE EAST ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 122. MIDDLE EAST ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 123. MIDDLE EAST ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 124. MIDDLE EAST ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 125. MIDDLE EAST ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 126. AFRICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

TABLE 127. AFRICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

TABLE 128. AFRICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

TABLE 129. AFRICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

TABLE 130. AFRICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

TABLE 131. MICROSOFT CORPORATION: KEY EXECUTIVES

TABLE 132. MICROSOFT CORPORATION: COMPANY SNAPSHOT

TABLE 133. MICROSOFT CORPORATION: SERVICE SEGMENTS

TABLE 134. MICROSOFT CORPORATION: PRODUCT PORTFOLIO

TABLE 135. MICROSOFT CORPORATION: KEY STRATERGIES

TABLE 136. INTERNATIONAL BUSINESS MACHINES CORPORATION: KEY EXECUTIVES

TABLE 137. INTERNATIONAL BUSINESS MACHINES CORPORATION: COMPANY SNAPSHOT

TABLE 138. INTERNATIONAL BUSINESS MACHINES CORPORATION: SERVICE SEGMENTS

TABLE 139. INTERNATIONAL BUSINESS MACHINES CORPORATION: PRODUCT PORTFOLIO

TABLE 140. INTERNATIONAL BUSINESS MACHINES CORPORATION: KEY STRATERGIES

TABLE 141. AMAZON WEB SERVICES, INC.: KEY EXECUTIVES

TABLE 142. AMAZON WEB SERVICES, INC.: COMPANY SNAPSHOT

TABLE 143. AMAZON WEB SERVICES, INC.: SERVICE SEGMENTS

TABLE 144. AMAZON WEB SERVICES, INC.: PRODUCT PORTFOLIO

TABLE 145. AMAZON WEB SERVICES, INC.: KEY STRATERGIES

TABLE 146. GOOGLE LLC: KEY EXECUTIVES

TABLE 147. GOOGLE LLC: COMPANY SNAPSHOT

TABLE 148. GOOGLE LLC: SERVICE SEGMENTS

TABLE 149. GOOGLE LLC: PRODUCT PORTFOLIO

TABLE 150. GOOGLE LLC: KEY STRATERGIES

TABLE 151. COGNIZANT: KEY EXECUTIVES

TABLE 152. COGNIZANT: COMPANY SNAPSHOT

TABLE 153. COGNIZANT: SERVICE SEGMENTS

TABLE 154. COGNIZANT: PRODUCT PORTFOLIO

TABLE 155. COGNIZANT: KEY STRATERGIES

TABLE 156. DREAMBOX LEARNING, INC.: KEY EXECUTIVES

TABLE 157. DREAMBOX LEARNING, INC.: COMPANY SNAPSHOT

TABLE 158. DREAMBOX LEARNING, INC.: SERVICE SEGMENTS

TABLE 159. DREAMBOX LEARNING, INC.: PRODUCT PORTFOLIO

TABLE 160. BRIDGEU: KEY EXECUTIVES

TABLE 161. BRIDGEU: COMPANY SNAPSHOT

TABLE 162. BRIDGEU: SERVICE SEGMENTS

TABLE 163. BRIDGEU: PRODUCT PORTFOLIO

TABLE 164. BRIDGEU: KEY STRATERGIES

TABLE 165. CARNEGIE LEARNING, INC.: KEY EXECUTIVES

TABLE 166. CARNEGIE LEARNING, INC.: COMPANY SNAPSHOT

TABLE 167. CARNEGIE LEARNING, INC.: SERVICE SEGMENTS

TABLE 168. CARNEGIE LEARNING, INC.: PRODUCT PORTFOLIO

TABLE 169. CARNEGIE LEARNING, INC.: KEY STRATERGIES

TABLE 170. PEARSON PLC: KEY EXECUTIVES

TABLE 171. PEARSON PLC: COMPANY SNAPSHOT

TABLE 172. PEARSON PLC: SERVICE SEGMENTS

TABLE 173. PEARSON PLC: PRODUCT PORTFOLIO

TABLE 174. PEARSON PLC: KEY STRATERGIES

TABLE 175. NUANCE COMMUNICATIONS, INC.: KEY EXECUTIVES

TABLE 176. NUANCE COMMUNICATIONS, INC.: COMPANY SNAPSHOT

TABLE 177. NUANCE COMMUNICATIONS, INC.: PRODUCT SEGMENTS

TABLE 178. NUANCE COMMUNICATIONS, INC.: PRODUCT PORTFOLIO

TABLE 179. NUANCE COMMUNICATIONS, INC.: KEY STRATERGIES LIST OF FIGURES

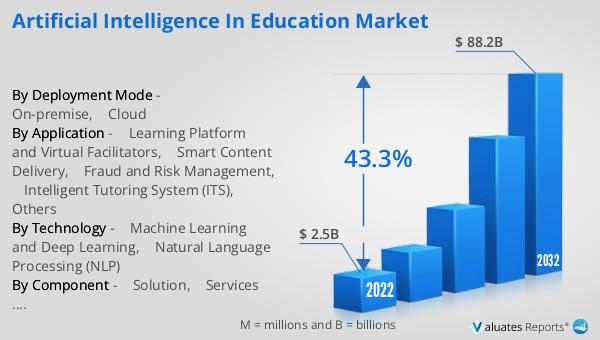

FIGURE 01. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032

FIGURE 02. SEGMENTATION OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032

FIGURE 03. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET,2022-2032

FIGURE 04. TOP INVESTMENT POCKETS IN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET (2023-2032)

FIGURE 05. LOW BARGAINING POWER OF SUPPLIERS

FIGURE 06. LOW THREAT OF NEW ENTRANTS

FIGURE 07. LOW THREAT OF SUBSTITUTES

FIGURE 08. LOW INTENSITY OF RIVALRY

FIGURE 09. LOW BARGAINING POWER OF BUYERS

FIGURE 10. GLOBAL ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

FIGURE 11. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022(%)

FIGURE 12. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR SOLUTION, BY COUNTRY 2022-2032(%)

FIGURE 13. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR SERVICES, BY COUNTRY 2022-2032(%)

FIGURE 14. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022(%)

FIGURE 15. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR ON-PREMISE, BY COUNTRY 2022-2032(%)

FIGURE 16. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR CLOUD, BY COUNTRY 2022-2032(%)

FIGURE 17. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022(%)

FIGURE 18. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR MACHINE LEARNING AND DEEP LEARNING, BY COUNTRY 2022-2032(%)

FIGURE 19. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR NATURAL LANGUAGE PROCESSING (NLP), BY COUNTRY 2022-2032(%)

FIGURE 20. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022(%)

FIGURE 21. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR LEARNING PLATFORM AND VIRTUAL FACILITATORS , BY COUNTRY 2022-2032(%)

FIGURE 22. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR SMART CONTENT DELIVERY, BY COUNTRY 2022-2032(%)

FIGURE 23. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR FRAUD AND RISK MANAGEMENT, BY COUNTRY 2022-2032(%)

FIGURE 24. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR INTELLIGENT TUTORING SYSTEM (ITS), BY COUNTRY 2022-2032(%)

FIGURE 25. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR OTHERS, BY COUNTRY 2022-2032(%)

FIGURE 26. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022(%)

FIGURE 27. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR HIGHER EDUCATION, BY COUNTRY 2022-2032(%)

FIGURE 28. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR K-12 EDUCATION, BY COUNTRY 2022-2032(%)

FIGURE 29. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR CORPORATE TRAINING AND LEARNING, BY COUNTRY 2022-2032(%)

FIGURE 30. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR OTHERS, BY COUNTRY 2022-2032(%)

FIGURE 31. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET BY REGION, 2022

FIGURE 32. U.S. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 33. CANADA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 34. UK ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 35. GERMANY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 36. FRANCE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 37. ITALY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 38. SPAIN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 39. REST OF EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 40. CHINA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 41. JAPAN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 42. INDIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 43. AUSTRALIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 44. SOUTH KOREA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 45. REST OF ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 46. LATIN AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 47. MIDDLE EAST ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 48. AFRICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

FIGURE 49. TOP WINNING STRATEGIES, BY YEAR

FIGURE 50. TOP WINNING STRATEGIES, BY DEVELOPMENT

FIGURE 51. TOP WINNING STRATEGIES, BY COMPANY

FIGURE 52. PRODUCT MAPPING OF TOP 10 PLAYERS

FIGURE 53. COMPETITIVE DASHBOARD

FIGURE 54. COMPETITIVE HEATMAP: ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET

FIGURE 55. TOP PLAYER POSITIONING, 2022

FIGURE 56. MICROSOFT CORPORATION: NET REVENUE, 2020-2022 ($MILLION)

FIGURE 57. INTERNATIONAL BUSINESS MACHINES CORPORATION: NET REVENUE, 2020-2022 ($MILLION)

FIGURE 58. INTERNATIONAL BUSINESS MACHINES CORPORATION: RESEARCH & DEVELOPMENT EXPENDITURE, 2019-2021 ($MILLION

FIGURE 59. INTERNATIONAL BUSINESS MACHINES CORPORATION: REVENUE SHARE BY REGION, 2022 (%)

FIGURE 60. INTERNATIONAL BUSINESS MACHINES CORPORATION: REVENUE SHARE BY SEGMENT, 2022 (%)

FIGURE 61. AMAZON WEB SERVICES, INC.: NET REVENUE, 2020-2022 ($MILLION)

FIGURE 62. AMAZON WEB SERVICES, INC.: REVENUE SHARE BY SEGMENT, 2022 (%)

FIGURE 63. AMAZON WEB SERVICES, INC.: REVENUE SHARE BY REGION, 2022 (%)

FIGURE 64. GOOGLE LLC: NET REVENUE, 2020-2022 ($MILLION)

FIGURE 65. GOOGLE LLC: RESEARCH & DEVELOPMENT EXPENDITURE, 2020-2022 ($MILLION)

FIGURE 66. GOOGLE LLC: REVENUE SHARE BY REGION, 2022 (%)

FIGURE 67. GOOGLE LLC: REVENUE SHARE BY SEGMENT, 2022 (%)

FIGURE 68. COGNIZANT: NET REVENUE, 2020-2022 ($MILLION)

FIGURE 69. COGNIZANT: REVENUE SHARE BY REGION, 2022 (%)

FIGURE 70. PEARSON PLC: NET REVENUE, 2020-2022 ($MILLION)

FIGURE 71. PEARSON PLC: REVENUE SHARE BY SEGMENT, 2022 (%)

FIGURE 72. PEARSON PLC: REVENUE SHARE BY REGION, 2022 (%)

FIGURE 73. NUANCE COMMUNICATIONS, INC.: NET REVENUE, 2020-2022 ($MILLION)

FIGURE 74. NUANCE COMMUNICATIONS, INC.: RESEARCH & DEVELOPMENT EXPENDITURE, 2020-2022 ($MILLION)

FIGURE 75. NUANCE COMMUNICATIONS, INC.: REVENUE SHARE BY SEGMENT, 2022 (%)

FIGURE 76. NUANCE COMMUNICATIONS, INC.: REVENUE SHARE BY REGION, 2022 (%