List of Tables

Table 1. Supercapacitors CAGR in Value, India VS Global, 2018 VS 2022 VS 2029

Table 2. Supercapacitors Market Trends

Table 3. Supercapacitors Market Drivers

Table 4. Supercapacitors Market Challenges

Table 5. Supercapacitors Market Restraints

Table 6. Global Supercapacitors Sales Growth Rate (CAGR) by Type: 2018 VS 2022 VS 2029 (US$ Million)

Table 7. India Supercapacitors Sales Growth Rate (CAGR) by Type: 2018 VS 2022 VS 2029 (US$ Million)

Table 8. Global Supercapacitors Sales Growth Rate (CAGR) by Application: 2018 VS 2022 VS 2029 (US$ Million)

Table 9. India Supercapacitors Sales Growth Rate (CAGR) by Application: 2018 VS 2022 VS 2029 (US$ Million)

Table 10. Global Key Manufacturers of Supercapacitors, Ranked by Revenue (2022) & (US$ Million)

Table 11. Global Supercapacitors Revenue by Manufacturer, (US$ Million), 2018-2023

Table 12. Global Supercapacitors Revenue Share by Manufacturer, 2018-2023

Table 13. Global Supercapacitors Sales by Manufacturer, (K Units), 2018-2023

Table 14. Global Supercapacitors Sales Share by Manufacturer, 2018-2023

Table 15. Global Supercapacitors Price by Manufacturer (2018-2023) & (USD/Unit)

Table 16. Global Supercapacitors Manufacturers Market Concentration Ratio (CR5 and HHI)

Table 17. Global Supercapacitors by Company Type (Tier 1, Tier 2, and Tier 3) & (based on the Revenue in Supercapacitors as of 2022)

Table 18. Global Key Manufacturers of Supercapacitors, Manufacturing Base Distribution and Headquarters

Table 19. Global Key Manufacturers of Supercapacitors, Product Offered and Application

Table 20. Global Key Manufacturers of Supercapacitors, Date of Enter into This Industry

Table 21. Manufacturers Mergers & Acquisitions, Expansion Plans

Table 22. Key Players of Supercapacitors in India, Ranked by Revenue (2022) & (US$ million)

Table 23. India Supercapacitors Revenue by Players, (US$ Million), (2018-2023)

Table 24. India Supercapacitors Revenue Share by Players, (2018-2023)

Table 25. India Supercapacitors Sales by Players, (K Units), (2018-2023)

Table 26. India Supercapacitors Sales Share by Players, (2018-2023)

Table 27. Global Supercapacitors Market Size Growth Rate (CAGR) by Region (US$ Million): 2018 VS 2022 VS 2029

Table 28. Global Supercapacitors Sales in Volume by Region (2018-2023) & (K Units)

Table 29. Global Supercapacitors Sales in Volume Forecast by Region (2024-2029) & (K Units)

Table 30. Global Supercapacitors Sales in Value by Region (2018-2023) & (US$ Million)

Table 31. Global Supercapacitors Sales in Value Forecast by Region (2024-2029) & (US$ Million)

Table 32. Americas Supercapacitors Market Size Growth Rate (CAGR) by Country (US$ Million): 2018 VS 2022 VS 2029

Table 33. Americas Supercapacitors Sales in Value by Country (2018-2023) & (US$ Million)

Table 34. Americas Supercapacitors Sales in Value by Country (2024-2029) & (US$ Million)

Table 35. Americas Supercapacitors Sales in Volume by Country (2018-2023) & (K Units)

Table 36. Americas Supercapacitors Sales in Volume by Country (2024-2029) & (K Units)

Table 37. EMEA Supercapacitors Market Size Growth Rate (CAGR) by Country (US$ Million): 2018 VS 2022 VS 2029

Table 38. EMEA Supercapacitors Sales in Value by Country (2018-2023) & (US$ Million)

Table 39. EMEA Supercapacitors Sales in Value by Country (2024-2029) & (US$ Million)

Table 40. EMEA Supercapacitors Sales in Volume by Country (2018-2023) & (K Units)

Table 41. EMEA Supercapacitors Sales in Volume by Country (2024-2029) & (K Units)

Table 42. APAC Supercapacitors Market Size Growth Rate (CAGR) by Country (US$ Million): 2018 VS 2022 VS 2029

Table 43. APAC Supercapacitors Sales in Value by Country (2018-2023) & (US$ Million)

Table 44. APAC Supercapacitors Sales in Value by Country (2024-2029) & (US$ Million)

Table 45. APAC Supercapacitors Sales in Volume by Country (2018-2023) & (K Units)

Table 46. APAC Supercapacitors Sales in Volume by Country (2024-2029) & (K Units)

Table 47. Maxwell Company Information

Table 48. Maxwell Description and Business Overview

Table 49. Maxwell Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 50. Maxwell Supercapacitors Product

Table 51. Maxwell Recent Development

Table 52. Panasonic Company Information

Table 53. Panasonic Description and Business Overview

Table 54. Panasonic Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 55. Panasonic Supercapacitors Product

Table 56. Panasonic Recent Development

Table 57. NEC TOKIN Company Information

Table 58. NEC TOKIN Description and Business Overview

Table 59. NEC TOKIN Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 60. NEC TOKIN Supercapacitors Product

Table 61. NEC TOKIN Recent Development

Table 62. Nesscap Company Information

Table 63. Nesscap Description and Business Overview

Table 64. Nesscap Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 65. Nesscap Supercapacitors Product

Table 66. Nesscap Recent Development

Table 67. AVX Company Information

Table 68. AVX Description and Business Overview

Table 69. AVX Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 70. AVX Supercapacitors Product

Table 71. AVX Recent Development

Table 72. ELNA Company Information

Table 73. ELNA Description and Business Overview

Table 74. ELNA Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 75. ELNA Supercapacitors Product

Table 76. ELNA Recent Development

Table 77. Korchip Company Information

Table 78. Korchip Description and Business Overview

Table 79. Korchip Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 80. Korchip Supercapacitors Product

Table 81. Korchip Recent Development

Table 82. Nippon Chemi-Con Company Information

Table 83. Nippon Chemi-Con Description and Business Overview

Table 84. Nippon Chemi-Con Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 85. Nippon Chemi-Con Supercapacitors Product

Table 86. Nippon Chemi-Con Recent Development

Table 87. Ioxus Company Information

Table 88. Ioxus Description and Business Overview

Table 89. Ioxus Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 90. Ioxus Supercapacitors Product

Table 91. Ioxus Recent Development

Table 92. LS Mtron Company Information

Table 93. LS Mtron Description and Business Overview

Table 94. LS Mtron Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 95. LS Mtron Supercapacitors Product

Table 96. LS Mtron Recent Development

Table 97. Nichicon Company Information

Table 98. Nichicon Description and Business Overview

Table 99. Nichicon Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 100. Nichicon Supercapacitors Product

Table 101. Nichicon Recent Development

Table 102. Shenzhen Technology Innovation Green (TIG) Company Information

Table 103. Shenzhen Technology Innovation Green (TIG) Description and Business Overview

Table 104. Shenzhen Technology Innovation Green (TIG) Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 105. Shenzhen Technology Innovation Green (TIG) Supercapacitors Product

Table 106. Shenzhen Technology Innovation Green (TIG) Recent Development

Table 107. VinaTech Company Information

Table 108. VinaTech Description and Business Overview

Table 109. VinaTech Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 110. VinaTech Supercapacitors Product

Table 111. VinaTech Recent Development

Table 112. Jinzhou Kaimei Power Company Information

Table 113. Jinzhou Kaimei Power Description and Business Overview

Table 114. Jinzhou Kaimei Power Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 115. Jinzhou Kaimei Power Supercapacitors Product

Table 116. Jinzhou Kaimei Power Recent Development

Table 117. Samwha Company Information

Table 118. Samwha Description and Business Overview

Table 119. Samwha Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 120. Samwha Supercapacitors Product

Table 121. Samwha Recent Development

Table 122. Haerbin Jurong Newpower Company Information

Table 123. Haerbin Jurong Newpower Description and Business Overview

Table 124. Haerbin Jurong Newpower Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 125. Haerbin Jurong Newpower Supercapacitors Product

Table 126. Haerbin Jurong Newpower Recent Development

Table 127. Ningbo CRRC New Energy Technology Company Information

Table 128. Ningbo CRRC New Energy Technology Description and Business Overview

Table 129. Ningbo CRRC New Energy Technology Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 130. Ningbo CRRC New Energy Technology Supercapacitors Product

Table 131. Ningbo CRRC New Energy Technology Recent Development

Table 132. Beijing HCC Energy Company Information

Table 133. Beijing HCC Energy Description and Business Overview

Table 134. Beijing HCC Energy Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 135. Beijing HCC Energy Supercapacitors Product

Table 136. Beijing HCC Energy Recent Development

Table 137. Jianghai Capacitor Company Information

Table 138. Jianghai Capacitor Description and Business Overview

Table 139. Jianghai Capacitor Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 140. Jianghai Capacitor Supercapacitors Product

Table 141. Jianghai Capacitor Recent Development

Table 142. Supreme Power Solutions Company Information

Table 143. Supreme Power Solutions Description and Business Overview

Table 144. Supreme Power Solutions Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 145. Supreme Power Solutions Supercapacitors Product

Table 146. Supreme Power Solutions Recent Development

Table 147. Shanghai Aowei Technology Company Information

Table 148. Shanghai Aowei Technology Description and Business Overview

Table 149. Shanghai Aowei Technology Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 150. Shanghai Aowei Technology Supercapacitors Product

Table 151. Shanghai Aowei Technology Recent Development

Table 152. Heter Electronics Company Information

Table 153. Heter Electronics Description and Business Overview

Table 154. Heter Electronics Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 155. Heter Electronics Supercapacitors Product

Table 156. Heter Electronics Recent Development

Table 157. CAP-XX Company Information

Table 158. CAP-XX Description and Business Overview

Table 159. CAP-XX Supercapacitors Sales (K Units), Revenue (US$ Million), Price (USD/Unit) and Gross Margin (2018-2023)

Table 160. CAP-XX Supercapacitors Product

Table 161. CAP-XX Recent Development

Table 162. Key Raw Materials Lists

Table 163. Raw Materials Key Suppliers Lists

Table 164. Supercapacitors Customers List

Table 165. Supercapacitors Distributors List

Table 166. Research Programs/Design for This Report

Table 167. Key Data Information from Secondary Sources

Table 168. Key Data Information from Primary Sources

List of Figures

Figure 1. Supercapacitors Product Picture

Figure 2. Global Supercapacitors Revenue, (US$ Million), 2018 VS 2022 VS 2029

Figure 3. Global Supercapacitors Market Size 2018-2029 (US$ Million)

Figure 4. Global Supercapacitors Sales 2018-2029 (K Units)

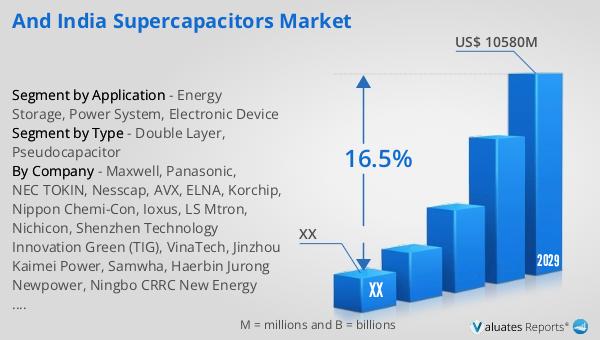

Figure 5. India Supercapacitors Revenue, (US$ Million), 2018 VS 2022 VS 2029

Figure 6. India Supercapacitors Market Size 2018-2029 (US$ Million)

Figure 7. India Supercapacitors Sales 2018-2029 (K Units)

Figure 8. India Supercapacitors Market Share in Global, in Value (US$ Million) 2018-2029

Figure 9. India Supercapacitors Market Share in Global, in Volume (K Units) 2018-2029

Figure 10. Supercapacitors Report Years Considered

Figure 11. Product Picture of Double Layer

Figure 12. Product Picture of Pseudocapacitor

Figure 13. Global Supercapacitors Market Share by Type in 2022 & 2029

Figure 14. Global Supercapacitors Sales in Value by Type (2018-2029) & (US$ Million)

Figure 15. Global Supercapacitors Sales Market Share in Value by Type (2018-2029)

Figure 16. Global Supercapacitors Sales by Type (2018-2029) & (K Units)

Figure 17. Global Supercapacitors Sales Market Share in Volume by Type (2018-2029)

Figure 18. Global Supercapacitors Price by Type (2018-2029) & (USD/Unit)

Figure 19. India Supercapacitors Market Share by Type in 2022 & 2029

Figure 20. India Supercapacitors Sales in Value by Type (2018-2029) & (US$ Million)

Figure 21. India Supercapacitors Sales Market Share in Value by Type (2018-2029)

Figure 22. India Supercapacitors Sales by Type (2018-2029) & (K Units)

Figure 23. India Supercapacitors Sales Market Share in Volume by Type (2018-2029)

Figure 24. India Supercapacitors Price by Type (2018-2029) & (USD/Unit)

Figure 25. Product Picture of Energy Storage

Figure 26. Product Picture of Power System

Figure 27. Product Picture of Electronic Device

Figure 28. Global Supercapacitors Market Share by Application in 2022 & 2029

Figure 29. Global Supercapacitors Sales in Value by Application (2018-2029) & (US$ Million)

Figure 30. Global Supercapacitors Sales Market Share in Value by Application (2018-2029)

Figure 31. Global Supercapacitors Sales by Application (2018-2029) & (K Units)

Figure 32. Global Supercapacitors Sales Market Share in Volume by Application (2018-2029)

Figure 33. Global Supercapacitors Price by Application (2018-2029) & (USD/Unit)

Figure 34. India Supercapacitors Market Share by Application in 2022 & 2029

Figure 35. India Supercapacitors Sales in Value by Application (2018-2029) & (US$ Million)

Figure 36. India Supercapacitors Sales Market Share in Value by Application (2018-2029)

Figure 37. India Supercapacitors Sales by Application (2018-2029) & (K Units)

Figure 38. India Supercapacitors Sales Market Share in Volume by Application (2018-2029)

Figure 39. India Supercapacitors Price by Application (2018-2029) & (USD/Unit)

Figure 40. Americas Supercapacitors Sales in Volume Growth Rate 2018-2029 (K Units)

Figure 41. Americas Supercapacitors Sales in Value Growth Rate 2018-2029 (US$ Million)

Figure 42. Americas Supercapacitors Sales by Type (2018-2029) & (K Units)

Figure 43. Americas Supercapacitors Sales Market Share in Volume by Type (2018-2029)

Figure 44. Americas Supercapacitors Sales by Application (2018-2029) & (K Units)

Figure 45. Americas Supercapacitors Sales Market Share in Volume by Application (2018-2029)

Figure 46. United States Supercapacitors Sales in Value Growth Rate (2018-2029) & (US$ Million)

Figure 47. Canada Supercapacitors Sales in Value Growth Rate (2018-2029) & (US$ Million)

Figure 48. Mexico Supercapacitors Sales in Value Growth Rate (2018-2029) & (US$ Million)

Figure 49. Brazil Supercapacitors Sales in Value Growth Rate (2018-2029) & (US$ Million)

Figure 50. EMEA Supercapacitors Sales in Volume Growth Rate 2018-2029 (K Units)

Figure 51. EMEA Supercapacitors Sales in Value Growth Rate 2018-2029 (US$ Million)

Figure 52. EMEA Supercapacitors Sales by Type (2018-2029) & (K Units)

Figure 53. EMEA Supercapacitors Sales Market Share in Volume by Type (2018-2029)

Figure 54. EMEA Supercapacitors Sales by Application (2018-2029) & (K Units)

Figure 55. EMEA Supercapacitors Sales Market Share in Volume by Application (2018-2029)

Figure 56. Europe Supercapacitors Sales in Value Growth Rate (2018-2029) & (US$ Million)

Figure 57. Middle East Supercapacitors Sales in Value Growth Rate (2018-2029) & (US$ Million)

Figure 58. Africa Supercapacitors Sales in Value Growth Rate (2018-2029) & (US$ Million)

Figure 59. China Supercapacitors Sales in Volume Growth Rate 2018-2029 (K Units)

Figure 60. China Supercapacitors Sales in Value Growth Rate 2018-2029 (US$ Million)

Figure 61. China Supercapacitors Sales by Type (2018-2029) & (K Units)

Figure 62. China Supercapacitors Sales Market Share in Volume by Type (2018-2029)

Figure 63. China Supercapacitors Sales by Application (2018-2029) & (K Units)

Figure 64. China Supercapacitors Sales Market Share in Volume by Application (2018-2029)

Figure 65. APAC Supercapacitors Sales in Volume Growth Rate 2018-2029 (K Units)

Figure 66. APAC Supercapacitors Sales in Value Growth Rate 2018-2029 (US$ Million)

Figure 67. APAC Supercapacitors Sales by Type (2018-2029) & (K Units)

Figure 68. APAC Supercapacitors Sales Market Share in Volume by Type (2018-2029)

Figure 69. APAC Supercapacitors Sales by Application (2018-2029) & (K Units)

Figure 70. APAC Supercapacitors Sales Market Share in Volume by Application (2018-2029)

Figure 71. Japan Supercapacitors Sales in Value Growth Rate (2018-2029) & (US$ Million)

Figure 72. South Korea Supercapacitors Sales in Value Growth Rate (2018-2029) & (US$ Million)

Figure 73. China Taiwan Supercapacitors Sales in Value Growth Rate (2018-2029) & (US$ Million)

Figure 74. Southeast Asia Supercapacitors Sales in Value Growth Rate (2018-2029) & (US$ Million)

Figure 75. India Supercapacitors Sales in Value Growth Rate (2018-2029) & (US$ Million)

Figure 76. Supercapacitors Value Chain

Figure 77. Supercapacitors Production Process

Figure 78. Channels of Distribution

Figure 79. Distributors Profiles

Figure 80. Bottom-up and Top-down Approaches for This Report

Figure 81. Data Triangulation

Figure 82. Key Executives Interviewed