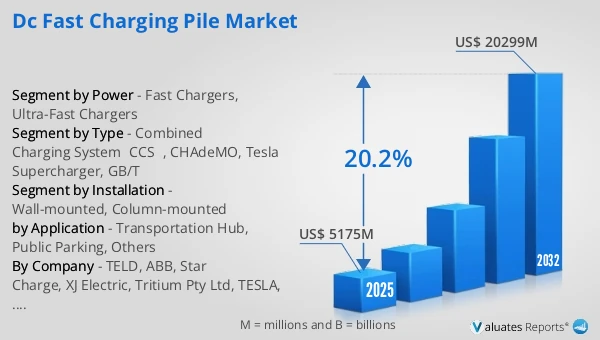

The global DC Fast Charging Pile market was valued at US$ 5175 million in 2025 and is anticipated to reach US$ 20299 million by 2032, at a CAGR of 20.2% from 2026 to 2032.

DC Fast Charging Pile Market

The 2025 U.S. tariff policies introduce profound uncertainty into the global economic landscape. This report critically examines the implications of recent tariff adjustments and international strategic countermeasures on DC Fast Charging Pile competitive dynamics, regional economic interdependencies, and supply chain reconfigurations.

DC fast charging piles are significantly faster than regular AC charging stations taking between 15 and 45 minutes to charge most passenger electric vehicles up to 80 percent—making it quick and easy to charge on the go. The DC fast chargers can range in output from 25 kW to 350 kW.

The upstream segment includes power semiconductors (Si/SiC), magnetic devices, capacitors, contactors/relays, liquid cooling components (for high power applications), and metering and communication modules; and the downstream segment includes charging point operators (CPOs), gas stations/supermarkets/parking lot operators, fleet and industrial park operators, and power grid/energy service providers.

In 2025, global DC fast charging piles production reached approximately 750 k units, with an average global market price is around $7,000 per unit.

DC fast charging piles market is a foundational segment of electric mobility infrastructure, enabling rapid energy replenishment for public charging, highway corridors, and fleet operations. As EV penetration rises, long-range models become mainstream, and high-frequency use cases expand, DC fast charging is shifting from a supplemental amenity to a reliability-driven network asset—positioned at the intersection of automaker ecosystems, grid capacity planning, and mobility services.

From a technology and product perspective, DC fast charging is evolving from early 50–60 kW deployments toward 150–350 kW ultra-fast charging as the dominant public-facing power band, with continued progress toward higher-voltage architectures, higher-current delivery, and megawatt-class solutions for heavy-duty vehicles. This shift is accompanied by a more engineered system architecture: the market is moving from all-in-one units to cabinet-plus-dispenser designs with shared power and dynamic power allocation, improving concurrency and site utilization. At higher power levels, liquid-cooled cables, stronger thermal management, and enhanced insulation and protection features become increasingly critical. In parallel, software has moved to the center of the value proposition—remote monitoring, diagnostics, billing, predictive maintenance, and site energy management are turning DCFC into a combined hardware–software–service offering rather than a one-time equipment sale.

Regionally, global deployment is concentrated in a handful of leading markets. Asia—especially China—continues to dominate in installed base and annual additions. Europe is accelerating corridor build-outs and high-power site density to support long-distance travel and cross-border mobility. North America is undergoing a notable shift in connector ecosystems and network access arrangements, which is driving compatibility retrofits and influencing new equipment specifications. In practice, regional differentiation is defined not only by installation counts, but by grid interconnection conditions, electricity pricing structures, utilization rates, and operator capability in uptime and user experience.

Key opportunities are emerging along three tracks. First, ultra-fast charging improves the predictability of "time-to-energy," supporting highway and urban-hub densification while boosting fleet turnaround efficiency. Second, fleets and commercial depots are increasingly optimizing total cost of ownership, accelerating integrated depot solutions that combine dedicated infrastructure, load management, and time-of-use strategies. Third, evolving connector ecosystems and interoperability expectations are generating upgrade and retrofit demand while raising the premium on system engineering and operational excellence for both equipment providers and network operators.

The DC fast charging market currently operates under multiple disparate standards (such as CCS in Europe/North America, legacy CHAdeMO, China's GB/T, and evolving ChaoJi/NACS initiatives), and these standards differ in connector form factors, communication protocols, and electrical interfaces, creating interoperability challenges. As a result, charging stations must plan for multi‑standard hardware, adapters, or retrofit costs at the design stage, increasing upfront capital expenditure and operational complexity while fragmenting the user experience.

This report delivers a comprehensive overview of the global DC Fast Charging Pile market, with both quantitative and qualitative analyses, to help readers develop growth strategies, assess the competitive landscape, evaluate their position in the current market, and make informed business decisions regarding DC Fast Charging Pile. The DC Fast Charging Pile market size, estimates, and forecasts are provided in terms of output/shipments (Units) and revenue (US$ millions), with 2025 as the base year and historical and forecast data for 2021–2032.

The report segments the global DC Fast Charging Pile market comprehensively. Regional market sizes by Type, by Application, by Power, and by company are also provided. For deeper insight, the report profiles the competitive landscape, key competitors, and their respective market rankings, and discusses technological trends and new product developments.

This report will assist DC Fast Charging Pile manufacturers, new entrants, and companies across the industry value chain with information on revenues, production, and average prices for the overall market and its sub-segments, by company, by Type, by Application, and by region.

Market Segmentation

Scope of DC Fast Charging Pile Market Report

| Report Metric |

Details |

| Report Name |

DC Fast Charging Pile Market |

| Accounted market size in 2025 |

US$ 5175 in million |

| Forecasted market size in 2032 |

US$ 20299 million |

| CAGR |

20.2% |

| Base Year |

2025 |

| Forecasted years |

2026 - 2032 |

| Segment by Type |

- Combined Charging System(CCS)

- CHAdeMO

- Tesla Supercharger

- GB/T

|

| Segment by Power |

- Fast Chargers

- Ultra-Fast Chargers

|

| Segment by Installation |

- Wall-mounted

- Column-mounted

|

| by Application |

- Transportation Hub

- Public Parking

- Others

|

| Production by Region |

- North America

- Europe

- China

- South Korea

|

| Consumption by Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia)

- Asia-Pacific (China, Japan, South Korea, Taiwan)

- Southeast Asia (India)

- Latin America (Mexico, Brazil)

|

| By Company |

TELD, ABB, Star Charge, XJ Electric, Tritium Pty Ltd, TESLA, ChargePoint, Efacec, Schneider Electric, Wanma, Siemens, BTC Power, Sinexcel |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |

Chapter Outline

- Chapter 1: Defines the scope of the report and presents an executive summary of market segments (by Type, by Application, by Power, etc.), including the size of each segment and its future growth potential. It offers a high-level view of the current market and its likely evolution in the short, medium, and long term.

- Chapter 2: Provides a detailed analysis of the competitive landscape for DC Fast Charging Pile manufacturers, including prices, production, value-based market shares, latest development plans, and information on mergers and acquisitions.

- Chapter 3: Examines DC Fast Charging Pile production/output and value by region and country, providing a quantitative assessment of market size and growth potential for each region over the next six years.

- Chapter 4: Analyzes DC Fast Charging Pile consumption at the regional and country levels. It quantifies market size and growth potential for each region and its key countries, and outlines market development, outlook, addressable space, and national production.

- Chapter 5: Analyzes market segments by Type, covering the size and growth potential of each segment to help readers identify “blue ocean” opportunities.

- Chapter 6: Analyzes market segments by Application, covering the size and growth potential of each segment to help readers identify “blue ocean” opportunities in downstream markets.

- Chapter 7: Profiles key players, detailing the fundamentals of major companies, including product production/output, value, price, gross margin, product portfolio/introductions, and recent developments.

- Chapter 8: Reviews the industry value chain, including upstream and downstream segments.

- Chapter 9: Discusses market dynamics and recent developments, including drivers, restraints, challenges and risks for manufacturers, U.S. Tariffs and relevant policy analysis.

- Chapter 10: Summarizes the key findings and conclusions of the report.

Ans: The DC Fast Charging Pile Market witnessing a CAGR of 20.2% during the forecast period 2026-2032.

Ans: The DC Fast Charging Pile Market size in 2032 will be US$ 20299 million.

Ans: The main players in the DC Fast Charging Pile Market are TELD, ABB, Star Charge, XJ Electric, Tritium Pty Ltd, TESLA, ChargePoint, Efacec, Schneider Electric, Wanma, Siemens, BTC Power, Sinexcel

Ans: The Applications covered in the DC Fast Charging Pile Market report are Transportation Hub, Public Parking, Others

Ans: The Types covered in the DC Fast Charging Pile Market report are Combined Charging System(CCS), CHAdeMO, Tesla Supercharger, GB/T