Semiconductor Equipment for BEOL Market Size

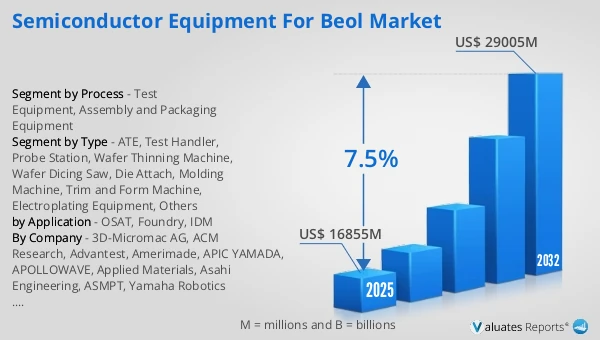

The global Semiconductor Equipment for BEOL market was valued at US$ 16855 million in 2025 and is anticipated to reach US$ 29005 million by 2032, at a CAGR of 7.5% from 2026 to 2032.

Semiconductor Equipment for BEOL Market

The 2025 U.S. tariff policies introduce profound uncertainty into the global economic landscape. This report critically examines the implications of recent tariff adjustments and international strategic countermeasures on Semiconductor Equipment for BEOL competitive dynamics, regional economic interdependencies, and supply chain reconfigurations.

Semiconductor back-end equipment (BEOL equipment) refers to the collective term for various process and testing equipment used throughout the entire process from wafer dicing to finished chip testing and warehousing after wafer manufacturing is completed. Its core function is to transform the bare chips (dies) manufactured in the front-end processes into functional, high-reliability chips that can be directly applied to end products through processes such as packaging, interconnection, and testing. Back-end processes cover four core stages: wafer-level packaging (WLP), chip assembly, packaging molding, and end-product testing.

Semiconductor Equipment for BEOL is further divided into A&P equipment and test equipment.

The global market for semiconductor back-end packaging equipment is in a cycle of robust recovery coupled with structural upgrading, driven by dual growth engines: it not only relies on the fundamental demand support from the global expansion of semiconductor production capacity, but also benefits from the technological transformation dividends brought by the iteration of AI and HPC chips. As a result, its overall growth resilience and rate have significantly outperformed the average level of the semiconductor equipment industry. The core logic of this market has undergone a fundamental shift. According to a joint study by SEMI and SIA, the focus of market drivers has gradually shifted from cost optimization in traditional packaging processes to performance breakthroughs in advanced packaging technologies. The large-scale industrialization of technologies such as Chiplet, 2.5D/3D packaging, hybrid bonding and through-silicon via (TSV) has completely reshaped the demand structure of back-end equipment, transforming the packaging segment from a passively supporting "cost center" in the past into a "value core" that determines the integration level, reliability and core performance of chips. Among these drivers, the explosive demand for AI chips and high-bandwidth memory (HBM) has emerged as a key growth engine. AI chips are driving the evolution of chip architectures toward heterogeneous integration, while HBM relies on multi-layer wafer stacking and high-precision interconnection processes. Together, they have fueled a surge in demand for high-end packaging equipment such as hybrid bonding systems, thermocompression bonding (TCB) equipment and wafer thinning machines. Meanwhile, as AI chips become more functionally complex and require more comprehensive verification dimensions, testing equipment has experienced a period of explosive growth, further boosting the growth momentum of the back-end market. In terms of market structure, back-end equipment has clearly split into two major categories: packaging process equipment and inspection & testing equipment. Leveraging its core role in yield control and performance verification, testing equipment has seen a steady rise in its value proportion. Within the packaging equipment segment, there is a clear trend of high-end differentiation—specialized equipment adapted to advanced packaging technologies is growing at a much faster pace than traditional standardized equipment, making it a core contributor to market growth. From a regional perspective, the Asia-Pacific region dominates the global market by virtue of its complete packaging and testing industrial chain ecosystem and production capacity agglomeration advantages. As the world's fastest-growing niche market, mainland China benefits both from the capacity expansion wave of local outsourced semiconductor assembly and test (OSAT) providers and wafer foundries, and forms a unique growth logic supported by the policy and industrial dividends of localization replacement. At present, local enterprises are gradually breaking through technical bottlenecks, penetrating from mature-process equipment to high-end segments such as hybrid bonding and TCB, and driving the market competition pattern to evolve from long-term monopoly by Japanese and American manufacturers toward a diversified, multi-echelon competitive landscape.

As an important branch of the semiconductor equipment ecosystem, semiconductor back-end testing equipment shares the overall development trend of back-end equipment while exhibiting distinct segment-specific characteristics. In terms of the global regional distribution of sales, market resources are highly concentrated in two major regions: mainland China and Taiwan, China. In 2024, their combined market share exceeded 60%. This pattern is highly aligned with the production capacity scale and industrial agglomeration degree of the packaging and testing industry chains in these two regions, and also reflects the long-term trend of the global semiconductor manufacturing and packaging & testing segments shifting to the Asia-Pacific region. However, from the perspective of supply chain autonomy and controllability, the self-sufficiency rate of local back-end testing equipment in China remains relatively low. The high-end market has long been dominated by enterprises from Japan and other countries. Gaps in core technologies, precision manufacturing capabilities and brand reputation have made it difficult for local enterprises to penetrate high-end segments such as probers and automatic test equipment (ATE). Nevertheless, in recent years, supported by favorable national industrial policies and the rapid development of the domestic semiconductor industry, the sales scale of the back-end testing equipment market in mainland China has continued to expand. Local enterprises have gradually emerged and gained a foothold in the global market. Companies including Changchuan Technology, Beijing Huafeng Test & Control, Liandong Technology and Jinhaitong Technology have achieved breakthroughs in the mid-to-low-end market by virtue of their accurate grasp of local customer needs, cost-effective advantages and continuous investment in technological R&D. Some of their products have also entered the verification phase in the high-end market, steadily accelerating the process of localization replacement. From the perspective of downstream demand in the industrial chain, the customer base of back-end testing equipment has shown a diversified expansion trend, fully covering four core sectors: packaging and testing enterprises, independent testing foundries, IDM manufacturers and research institutions & universities. Among these, packaging and testing enterprises serve as the main force of the industry and account for the core procurement share. There are significant differences in demand among different customer groups: packaging and testing enterprises prioritize the stability, compatibility and batch testing efficiency of equipment; independent testing foundries focus on the flexible adaptability of equipment to handle multi-category orders; IDM manufacturers emphasize the customized matching between equipment and their own product processes; research institutions and universities demand small-sized, high-precision experimental equipment. This demand differentiation not only reflects the trend of continuous refinement of the division of labor in the semiconductor industry, but also forces equipment manufacturers to accelerate technological iteration and improve their product portfolios. With the popularization of advanced technologies such as 3D packaging and system-in-package (SiP), the technological development direction of back-end testing equipment has become increasingly clear, presenting core characteristics including an increase in the number of test channels, faster test speed, multi-functional module integration and higher test precision. Packaging and testing enterprises need to rely on high-precision testing equipment to meet the testing challenges of complex chips, and at the same time use big data analysis capabilities to optimize test processes and reduce unit test costs. Moreover, the co-development of equipment with multiple technical grades, along with the coordinated evolution of high-end and mid-to-low-end markets, has become one of the core development laws of the back-end testing equipment industry.

This report delivers a comprehensive overview of the global Semiconductor Equipment for BEOL market, with both quantitative and qualitative analyses, to help readers develop growth strategies, assess the competitive landscape, evaluate their position in the current market, and make informed business decisions regarding Semiconductor Equipment for BEOL. The Semiconductor Equipment for BEOL market size, estimates, and forecasts are provided in terms of output/shipments (Units) and revenue (US$ millions), with 2025 as the base year and historical and forecast data for 2021–2032.

The report segments the global Semiconductor Equipment for BEOL market comprehensively. Regional market sizes by Process, by Application, by Type, and by company are also provided. For deeper insight, the report profiles the competitive landscape, key competitors, and their respective market rankings, and discusses technological trends and new product developments.

This report will assist Semiconductor Equipment for BEOL manufacturers, new entrants, and companies across the industry value chain with information on revenues, production, and average prices for the overall market and its sub-segments, by company, by Process, by Application, and by region.

Market Segmentation

Scope of Semiconductor Equipment for BEOL Market Report

| Report Metric |

Details |

| Report Name |

Semiconductor Equipment for BEOL Market |

| Accounted market size in 2025 |

US$ 16855 million |

| Forecasted market size in 2032 |

US$ 29005 million |

| CAGR |

7.5% |

| Base Year |

2025 |

| Forecasted years |

2026 - 2032 |

| Segment by Process |

- Test Equipment

- Assembly and Packaging Equipment

|

| Segment by Type |

- ATE

- Test Handler

- Probe Station

- Wafer Thinning Machine

- Wafer Dicing Saw

- Die Attach

- Molding Machine

- Trim and Form Machine

- Electroplating Equipment

- Others

|

| by Application |

|

| Production by Region |

- North America

- Europe

- China

- Japan

- South Korea

- Southeast Asia

- China Taiwan

|

| Consumption by Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia)

- Asia-Pacific (China, Japan, South Korea, Taiwan)

- Southeast Asia (India)

- Latin America (Mexico, Brazil)

|

| By Company |

3D-Micromac AG, ACM Research, Advantest, Amerimade, APIC YAMADA, APOLLOWAVE, Applied Materials, Asahi Engineering, ASMPT, Yamaha Robotics (SHINKAWA), ATECO, Athlete FA, Beijing Huafeng Test & Control Technology, Besi, Boston Semi Equipment, Capcon Limited, CETC-45, Chroma ATE Inc, ClassOne Technology, Cohu, Dalian Jafeng Automation Co.,Ltd, DISCO, Dongguan Huayue Semiconductor Technology, Easy Field Corporation, Ecopia, Engis Corporation, EO Technics, ESDEMC Technology, Everbeing, Exatron, Fasford Technology, Finetech, Fittech, FormFactor, G&N, Genesem, GL Tech, Guangdong Qrobot, Guangzhou Great Chieftain Electronics Machinery, Hangzhou Changchuan Technology, HANMI Semiconductor, Han's Laser Technology Co, Hanwha Semitech Co., Ltd, Hesse GmbH, HIIG Trinity (Anhui) Technology, HiSOL,Inc, Hon Precision, Hunan Yujing Machine Industrial, I-PEX Inc, JHT Design Co.,Ltd, Jiangsu Guoxin Intelligent Equipment Co., Ltd, Kanematsu, KeithLink Technology, KeyFactor Systems, Koyo Machinery, Kulicke & Soffa, Lake Shore Cryotronics, Lam Research, Macrotest, MarTek, Micromanipulator, Micronics Japan, Microtec Handling Systems GmbH, MicroXact, Mirae Corporation, MPI Corporation, Mtex Matsumura, Mycronic, Nextool Technology Co., Ltd., NTS, Okamoto Semiconductor Equipment Division, Palomar Technologies, Panasonic, Pentamaster, PowerTECH, Ramgraber GmbH, RENA Technologies, Revasum, SEMES, Semics, SemiProbe, SESSCO Technologies, SET, Shanghai Cascol, Shanghai Sinyang, Shanghai Xinsheng, Shanghai YOUNG SOUL, Shenzhen Biaopu Semiconductor Technology, Shenzhen Cindbest Technology, Shenzhen Guangyuan Intelligent Equipment Co, Shenzhen Hi-Test Semiconductor Equipment Co., Ltd, Shenzhen Liande Automatic Equipment Co., Ltd, Shenzhen Semishare, Shibasoku, Shibuya Corporation, Sidea Semiconductor, Signatone Corporation, SPEA, SpeedFam, SUSS MicroTec, Suzhou Bopai Semiconductor (Boschman), Suzhou Delphi Laser Co, Suzhou Maxwell Technologies Co, Suzhou Quick Laser Technology Co, Suzhou Saiken Intelligent Technology, Suzhou Zhicheng Semiconductor Technology, SYNAX, Synova S.A., TANAKA Precious Metals, Technic, Techwing, TEL, Teradyne, Tesec Inc, TKC, TOKYO SEIMITSU (Accretech), Toray, Towa, TSD, UENO SEIKI NAGANO, Ultrasonic Engineering, WAIDA MFG, Wentworth Laboratories, Wuhan Huagong Laser Engineering Co, Wuhan Jingce Electronic Technology, Wuxi Autowell Technology Co, YC Corp |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |

Chapter Outline

- Chapter 1: Defines the scope of the report and presents an executive summary of market segments (by Process, by Application, by Type, etc.), including the size of each segment and its future growth potential. It offers a high-level view of the current market and its likely evolution in the short, medium, and long term.

- Chapter 2: Provides a detailed analysis of the competitive landscape for Semiconductor Equipment for BEOL manufacturers, including prices, production, value-based market shares, latest development plans, and information on mergers and acquisitions.

- Chapter 3: Examines Semiconductor Equipment for BEOL production/output and value by region and country, providing a quantitative assessment of market size and growth potential for each region over the next six years.

- Chapter 4: Analyzes Semiconductor Equipment for BEOL consumption at the regional and country levels. It quantifies market size and growth potential for each region and its key countries, and outlines market development, outlook, addressable space, and national production.

- Chapter 5: Analyzes market segments by Process, covering the size and growth potential of each segment to help readers identify “blue ocean” opportunities.

- Chapter 6: Analyzes market segments by Application, covering the size and growth potential of each segment to help readers identify “blue ocean” opportunities in downstream markets.

- Chapter 7: Profiles key players, detailing the fundamentals of major companies, including product production/output, value, price, gross margin, product portfolio/introductions, and recent developments.

- Chapter 8: Reviews the industry value chain, including upstream and downstream segments.

- Chapter 9: Discusses market dynamics and recent developments, including drivers, restraints, challenges and risks for manufacturers, U.S. Tariffs and relevant policy analysis.

- Chapter 10: Summarizes the key findings and conclusions of the report.

FAQ for this report

How fast is Semiconductor Equipment for BEOL Market growing?

Ans: The Semiconductor Equipment for BEOL Market witnessing a CAGR of 7.5% during the forecast period 2026-2032.

What is the Semiconductor Equipment for BEOL Market size in 2032?

Ans: The Semiconductor Equipment for BEOL Market size in 2032 will be US$ 29005 million.

Who are the main players in the Semiconductor Equipment for BEOL Market report?

Ans: The main players in the Semiconductor Equipment for BEOL Market are 3D-Micromac AG, ACM Research, Advantest, Amerimade, APIC YAMADA, APOLLOWAVE, Applied Materials, Asahi Engineering, ASMPT, Yamaha Robotics (SHINKAWA), ATECO, Athlete FA, Beijing Huafeng Test & Control Technology, Besi, Boston Semi Equipment, Capcon Limited, CETC-45, Chroma ATE Inc, ClassOne Technology, Cohu, Dalian Jafeng Automation Co.,Ltd, DISCO, Dongguan Huayue Semiconductor Technology, Easy Field Corporation, Ecopia, Engis Corporation, EO Technics, ESDEMC Technology, Everbeing, Exatron, Fasford Technology, Finetech, Fittech, FormFactor, G&N, Genesem, GL Tech, Guangdong Qrobot, Guangzhou Great Chieftain Electronics Machinery, Hangzhou Changchuan Technology, HANMI Semiconductor, Han's Laser Technology Co, Hanwha Semitech Co., Ltd, Hesse GmbH, HIIG Trinity (Anhui) Technology, HiSOL,Inc, Hon Precision, Hunan Yujing Machine Industrial, I-PEX Inc, JHT Design Co.,Ltd, Jiangsu Guoxin Intelligent Equipment Co., Ltd, Kanematsu, KeithLink Technology, KeyFactor Systems, Koyo Machinery, Kulicke & Soffa, Lake Shore Cryotronics, Lam Research, Macrotest, MarTek, Micromanipulator, Micronics Japan, Microtec Handling Systems GmbH, MicroXact, Mirae Corporation, MPI Corporation, Mtex Matsumura, Mycronic, Nextool Technology Co., Ltd., NTS, Okamoto Semiconductor Equipment Division, Palomar Technologies, Panasonic, Pentamaster, PowerTECH, Ramgraber GmbH, RENA Technologies, Revasum, SEMES, Semics, SemiProbe, SESSCO Technologies, SET, Shanghai Cascol, Shanghai Sinyang, Shanghai Xinsheng, Shanghai YOUNG SOUL, Shenzhen Biaopu Semiconductor Technology, Shenzhen Cindbest Technology, Shenzhen Guangyuan Intelligent Equipment Co, Shenzhen Hi-Test Semiconductor Equipment Co., Ltd, Shenzhen Liande Automatic Equipment Co., Ltd, Shenzhen Semishare, Shibasoku, Shibuya Corporation, Sidea Semiconductor, Signatone Corporation, SPEA, SpeedFam, SUSS MicroTec, Suzhou Bopai Semiconductor (Boschman), Suzhou Delphi Laser Co, Suzhou Maxwell Technologies Co, Suzhou Quick Laser Technology Co, Suzhou Saiken Intelligent Technology, Suzhou Zhicheng Semiconductor Technology, SYNAX, Synova S.A., TANAKA Precious Metals, Technic, Techwing, TEL, Teradyne, Tesec Inc, TKC, TOKYO SEIMITSU (Accretech), Toray, Towa, TSD, UENO SEIKI NAGANO, Ultrasonic Engineering, WAIDA MFG, Wentworth Laboratories, Wuhan Huagong Laser Engineering Co, Wuhan Jingce Electronic Technology, Wuxi Autowell Technology Co, YC Corp

What are the Application segmentation covered in the Semiconductor Equipment for BEOL Market report?

Ans: The Applications covered in the Semiconductor Equipment for BEOL Market report are OSAT, Foundry, IDM

What are the Type segmentation covered in the Semiconductor Equipment for BEOL Market report?

Ans: The Types covered in the Semiconductor Equipment for BEOL Market report are ATE, Test Handler, Probe Station, Wafer Thinning Machine, Wafer Dicing Saw, Die Attach, Molding Machine, Trim and Form Machine, Electroplating Equipment, Others