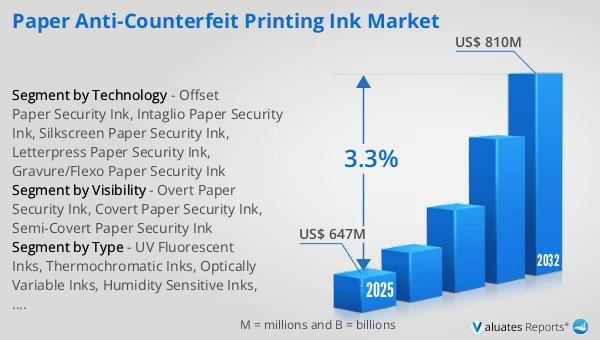

The global Paper Anti-Counterfeit Printing Ink market was valued at US$ 647 million in 2025 and is anticipated to reach US$ 810 million by 2032, at a CAGR of 3.3% from 2026 to 2032.

Paper Anti-Counterfeit Printing Ink Market

The 2025 U.S. tariff policies introduce profound uncertainty into the global economic landscape. This report critically examines the implications of recent tariff adjustments and international strategic countermeasures on Paper Anti-Counterfeit Printing Ink competitive dynamics, regional economic interdependencies, and supply chain reconfigurations.

Paper Anti-Counterfeit Printing Ink refers to security ink systems engineered specifically for paper-based substrates—such as security paper for IDs, certificates, tickets, revenue stamps, security labels, and paper packaging—providing verifiable, hard-to-replicate features that mitigate copying, scanning, alteration, wash-and-reprint attacks, and substitution of printed elements. Compared with general-purpose printing inks, these formulations emphasize compatibility with paper fibers, fillers, sizing and coating layers, and they are designed to remain stable under long-term storage, abrasion, folding, perspiration exposure, and common chemical contact. Depending on the security strategy, they can deliver overt effects (special colors, pearlescent/color-shift appearances, tactile features), covert and forensic effects (UV/IR response, magnetic signatures, machine-readable signals), and coordinated performance with security-paper elements such as watermarks, embedded security threads, security fibers, or chemically sensitive backgrounds for tiered authentication. Historically, paper security inks evolved alongside the broader “security paper + security printing” ecosystem—from early reliance on special pigments and invisible inks toward system-level solutions grounded in optical, magnetic, and materials engineering—driven by an ongoing arms race with increasingly sophisticated reproduction and tampering methods. Upstream inputs typically include binder/resin and vehicle platforms tuned for paper absorption and drying (oil-based and water-based systems, and in some cases UV-curable platforms), functional pigments and dyes (fluorescent/phosphorescent, IR, color-shift, magnetic, etc.), carriers/solvents, dispersion and rheology additives, abrasion and penetration-control additives, and substrate-matching primers and overprint varnishes; verification commonly relies on complementary components such as UV/IR illumination sources, optical filters, magnetic sensing heads, and vision/sensor-based readers supplied through the broader specialty materials and inspection equipment ecosystem.In 2025, global production capacity for paper anti-counterfeiting printing inks reached 250,000 tons, with sales volume totaling 189,500 tons. The average selling price was USD 3,415 per ton, and industry gross margins were generally in the range of 20%–30%.

The paper security-ink market remains anchored in the “security paper + security printing” ecosystem, characterized by high qualification barriers and long-term supplier relationships. In identity, fiscal, and official document use cases, inks are typically engineered to work in concert with security-paper features such as watermarks, embedded threads, security fibers, and chemically sensitive backgrounds; buyers prioritize traceable delivery, lot-to-lot consistency, long-term optical/chemical stability, and predictable performance within established processes such as intaglio, offset, and screen printing. At the same time, demand is expanding in commercial paper applications—labels, vouchers, tickets, certificates—where adoption favors solutions that integrate smoothly into existing workflows and support fast field inspection and channel audits. Overall, the market is moving from single covert effects toward tiered authentication that spans quick frontline checks as well as instrumented verification and evidentiary needs, making system capability and pressroom support a primary differentiator.

Future development will center on deeper feature integration, machine readability, and standardized verification. Technically, fluorescence will be combined more frequently with infrared, magnetic, color-shift, micro-structured, or taggant-based elements to create multi-channel features that are harder to imitate while preserving paper aesthetics and tactile feel. Operationally, paper-based credential security is increasingly expected to connect with digital governance—linking printed security marks with serialization, track-and-trace, regulatory reporting, or verification systems—so the paper feature becomes a recordable and auditable evidence point. From a quality and implementation perspective, greater cross-regional collaboration and outsourcing will increase the importance of harmonized acceptance criteria and test conditions (excitation wavelength, filters, decision thresholds, durability protocols) to reduce inconsistency across agencies and devices. In parallel, sustainability and compliance pressures will accelerate migration toward lower-VOC, low-odor, low-migration systems and more benign additive choices, especially for frequently handled documents and certain paper packaging contexts.

Key drivers include persistent demand to combat forgery and alteration, the dependence of fiscal and public-administration systems on trusted paper credentials, and rising risks of copying and misuse in cross-border and e-commerce environments. Brands also place growing value on the credibility of paper-based entitlement instruments and channel materials to reduce fraud and disputes. Constraints are largely implementation and lifecycle complexity: paper absorbency, coating structure, sizing, and filler variability can materially affect color and fluorescence, while post-press treatments (lamination, varnishing, embossing, thermal coatings) may change readability and lengthen qualification cycles. Non-uniform field tools, limited operator training, and the availability of low-end substitute materials can further erode single-feature effectiveness, pushing solutions toward multi-feature, system-level designs that raise cost and deployment thresholds. Competitive advantage will increasingly depend on balancing security strength, manufacturability at scale, consistent cross-institution verification, and sustainable compliance—while reducing customer friction through repeatable delivery and service models.

This report delivers a comprehensive overview of the global Paper Anti-Counterfeit Printing Ink market, with both quantitative and qualitative analyses, to help readers develop growth strategies, assess the competitive landscape, evaluate their position in the current market, and make informed business decisions regarding Paper Anti-Counterfeit Printing Ink. The Paper Anti-Counterfeit Printing Ink market size, estimates, and forecasts are provided in terms of output/shipments (Tons) and revenue (US$ millions), with 2025 as the base year and historical and forecast data for 2021–2032.

The report segments the global Paper Anti-Counterfeit Printing Ink market comprehensively. Regional market sizes by Type, by Application, by Visibility, and by company are also provided. For deeper insight, the report profiles the competitive landscape, key competitors, and their respective market rankings, and discusses technological trends and new product developments.

This report will assist Paper Anti-Counterfeit Printing Ink manufacturers, new entrants, and companies across the industry value chain with information on revenues, production, and average prices for the overall market and its sub-segments, by company, by Type, by Application, and by region.

Market Segmentation

Scope of Paper Anti-Counterfeit Printing Ink Market Report

| Report Metric |

Details |

| Report Name |

Paper Anti-Counterfeit Printing Ink Market |

| Accounted market size in 2025 |

US$ 647 million |

| Forecasted market size in 2032 |

US$ 810 million |

| CAGR |

3.3% |

| Base Year |

2025 |

| Forecasted years |

2026 - 2032 |

| Segment by Type |

- UV Fluorescent Inks

- Thermochromatic Inks

- Optically Variable Inks

- Humidity Sensitive Inks

- Infrared Fluorescent Inks

- Pressure Sensitive Inks

- Others

|

| Segment by Visibility |

- Overt Paper Security Ink

- Covert Paper Security Ink

- Semi-Covert Paper Security Ink

|

| Segment by Technology |

- Offset Paper Security Ink

- Intaglio Paper Security Ink

- Silkscreen Paper Security Ink

- Letterpress Paper Security Ink

- Gravure/Flexo Paper Security Ink

|

| by Application |

- Banknotes

- Official Identity Documents

- Tax Banderoles

- Security Labels

- Others

|

| Production by Region |

- North America

- Europe

- China

- Japan

|

| Consumption by Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia)

- Asia-Pacific (China, Japan, South Korea, Taiwan)

- Southeast Asia (India)

- Latin America (Mexico, Brazil)

|

| By Company |

SICPA, Sun Chemical, Luminescence Sun Chemical Security, Kao Collins, Angstrom Technologies, Flint Group, Microtrace, INX International Ink, ROTOFLEX, Gleitsmann Security Inks, PETREL, Cronite, Chroma Inks USA, hubergroup, artience, Shanghai Wancheng Anti-counterfeiting Ink, Mingbo Security Technology, GODO Printing Ink |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |

Chapter Outline

- Chapter 1: Defines the scope of the report and presents an executive summary of market segments (by Type, by Application, by Visibility, etc.), including the size of each segment and its future growth potential. It offers a high-level view of the current market and its likely evolution in the short, medium, and long term.

- Chapter 2: Provides a detailed analysis of the competitive landscape for Paper Anti-Counterfeit Printing Ink manufacturers, including prices, production, value-based market shares, latest development plans, and information on mergers and acquisitions.

- Chapter 3: Examines Paper Anti-Counterfeit Printing Ink production/output and value by region and country, providing a quantitative assessment of market size and growth potential for each region over the next six years.

- Chapter 4: Analyzes Paper Anti-Counterfeit Printing Ink consumption at the regional and country levels. It quantifies market size and growth potential for each region and its key countries, and outlines market development, outlook, addressable space, and national production.

- Chapter 5: Analyzes market segments by Type, covering the size and growth potential of each segment to help readers identify “blue ocean” opportunities.

- Chapter 6: Analyzes market segments by Application, covering the size and growth potential of each segment to help readers identify “blue ocean” opportunities in downstream markets.

- Chapter 7: Profiles key players, detailing the fundamentals of major companies, including product production/output, value, price, gross margin, product portfolio/introductions, and recent developments.

- Chapter 8: Reviews the industry value chain, including upstream and downstream segments.

- Chapter 9: Discusses market dynamics and recent developments, including drivers, restraints, challenges and risks for manufacturers, U.S. Tariffs and relevant policy analysis.

- Chapter 10: Summarizes the key findings and conclusions of the report.

Ans: The main players in the Paper Anti-Counterfeit Printing Ink Market are SICPA, Sun Chemical, Luminescence Sun Chemical Security, Kao Collins, Angstrom Technologies, Flint Group, Microtrace, INX International Ink, ROTOFLEX, Gleitsmann Security Inks, PETREL, Cronite, Chroma Inks USA, hubergroup, artience, Shanghai Wancheng Anti-counterfeiting Ink, Mingbo Security Technology, GODO Printing Ink

Ans: The Applications covered in the Paper Anti-Counterfeit Printing Ink Market report are Banknotes, Official Identity Documents, Tax Banderoles, Security Labels, Others

Ans: The Types covered in the Paper Anti-Counterfeit Printing Ink Market report are UV Fluorescent Inks, Thermochromatic Inks, Optically Variable Inks, Humidity Sensitive Inks, Infrared Fluorescent Inks, Pressure Sensitive Inks, Others