LIST OF TABLES

TABLE 01. GLOBAL SMART MOBILITY MARKET, BY ELEMENT, 2019-2027 ($MILLION)

TABLE 02. SMART MOBILITY MARKET REVENUE FOR BIKE COMMUTING, BY REGION 2019–2027 ($MILLION)

TABLE 03. SMART MOBILITY MARKET REVENUE FOR CAR SHARING, BY REGION 2019–2027 ($MILLION)

TABLE 04. SMART MOBILITY MARKET REVENUE FOR RIDESHARING, BY REGION 2019–2027 ($MILLION)

TABLE 05. GLOBAL SMART MOBILITY MARKET, BY SOLUTION, 2019-2027 ($MILLION)

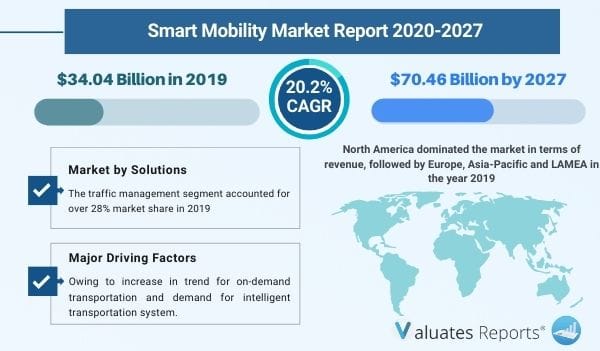

TABLE 06. SMART MOBILITY MARKET REVENUE FOR TRAFFIC MANAGEMENT, BY REGION 2019–2027 ($MILLION)

TABLE 07. SMART MOBILITY MARKET REVENUE FOR PARKING MANAGEMENT, BY REGION 2019–2027 ($MILLION)

TABLE 08. SMART MOBILITY MARKET REVENUE FOR MOBILITY MANAGEMENT, BY REGION 2019–2027 ($MILLION)

TABLE 09. SMART MOBILITY MARKET REVENUE FOR OTHERS, BY REGION 2019–2027 ($MILLION)

TABLE 10. GLOBAL SMART MOBILITY MARKET, BY TECHNOLOGY, 2019-2027 ($MILLION)

TABLE 11. SMART MOBILITY MARKET REVENUE FOR 3G & 4G, BY REGION 2019–2027 ($MILLION)

TABLE 12. SMART MOBILITY MARKET REVENUE FOR WI-FI, BY REGION 2019–2027 ($MILLION)

TABLE 13. SMART MOBILITY MARKET REVENUE FOR GNSS/GPS, BY REGION 2019–2027 ($MILLION)

TABLE 14. SMART MOBILITY MARKET REVENUE FOR RFID, BY REGION 2019–2027 ($MILLION)

TABLE 15. SMART MOBILITY MARKET REVENUE FOR EMBEDDED SYSTEMS, BY REGION 2019–2027 ($MILLION)

TABLE 16. SMART MOBILITY MARKET REVENUE FOR OTHERS, BY REGION 2019–2027 ($MILLION)

TABLE 17. NORTH AMERICA SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 18. NORTH AMERICA SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 19. NORTH AMERICA SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 20. U.S. SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 21. U.S. SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 22. U.S. SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 23. CANADA SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 24. CANADA SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 25. CANADA SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 26. MEXICO SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 27. MEXICO SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 28. MEXICO SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 29. EUROPE SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 30. EUROPE SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 31. EUROPE SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 32. GERMANY SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 33. GERMANY SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 34. GERMANY SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 35. FRANCE SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 36. FRANCE SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 37. FRANCE SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 38. UK SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 39. UK SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 40. UK SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 41. ITALY SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 42. ITALY SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 43. ITALY SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 44. REST OF EUROPE SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 45. REST OF EUROPE SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 46. REST OF EUROPE SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 47. ASIA-PACIFIC SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 48. ASIA-PACIFIC SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 49. ASIA-PACIFIC SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 50. CHINA SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 51. CHINA SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 52. CHINA SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 53. JAPAN SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 54. JAPAN SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 55. JAPAN SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 56. INDIA SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 57. INDIA SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 58. INDIA SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 59. SOUTH KOREA SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 60. SOUTH KOREA SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 61. SOUTH KOREA SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 62. REST OF ASIA-PACIFIC SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 63. REST OF ASIA-PACIFIC SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 64. REST OF ASIA-PACIFIC SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 65. LAMEA SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 66. LAMEA SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 67. LAMEA SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 68. LATIN AMERICA SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 69. LATIN AMERICA SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 70. LATIN AMERICA SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 71. MIDDLE EAST SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 72. MIDDLE EAST SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 73. MIDDLE EAST SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 74. AFRICA SMART MOBILITY MARKET, BY ELEMENTS, 2019–2027 ($MILLION)

TABLE 75. AFRICA SMART MOBILITY MARKET, BY SOLUTION, 2019–2027 ($MILLION)

TABLE 76. AFRICA SMART MOBILITY MARKET, BY TECHNOLOGY, 2019–2027 ($MILLION)

TABLE 77. CISCO SYSTEMS , INC.: COMPANY SNAPSHOT

TABLE 78. CISCO: PRODUCT PORTFOLIO

TABLE 79. CISCO: OPERATING SEGMENTS

TABLE 80. CISCO: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 81. EXCELFORE: COMPANY SNAPSHOT

TABLE 82. EXCELFORE: PRODUCT PORTFOLIO

TABLE 83. EXCELFORE: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 84. FORD MOTOR COMPANY: COMPANY SNAPSHOT

TABLE 85. FORD MOTOR COMPANY: PRODUCT PORTFOLIO

TABLE 86. FORD MOTOR COMPANY: OPERATING SEGMENTS

TABLE 87. FORD MOTOR COMPANY: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 88. INNOVIZ TECHNOLOGIES INC: COMPANY SNAPSHOT

TABLE 89. INNOVIZ TECHNOLOGIES INC: PRODUCT PORTFOLIO

TABLE 90. INNOVIZ TECHNOLOGIES INC: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 91. MAAS GLOBAL OY: COMPANY SNAPSHOT

TABLE 92. MAAS GLOBAL OY: PRODUCT PORTFOLIO

TABLE 93. QUALIX INFORMATION SYSTEM: COMPANY SNAPSHOT

TABLE 94. QUALIX INFORMATION SYSTEM: PRODUCT PORTFOLIO

TABLE 95. ROBERT BOSCH GMBH: COMPANY SNAPSHOT

TABLE 96. ROBERT BOSCH GMBH: PRODUCT PORTFOLIO

TABLE 97. ROBERT BOSCH GMBH: OPERATING SEGMENTS

TABLE 98. ROBERT BOSCH GMBH: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 99. SIEMENS: COMPANY SNAPSHOT

TABLE 100. SIEMENS: PRODUCT PORTFOLIO

TABLE 101. SIEMENS: OPERATING SEGMENTS

TABLE 102. TOMTOM INTERNATIONAL N.V.: COMPANY SNAPSHOT

TABLE 103. TOMTOM INTERNATIONAL N.V.: OPERATING SEGMENTS

TABLE 104. TOMTOM INTERNATIONAL N.V.: PRODUCT PORTFOLIO

TABLE 105. TOMTOM INTERNATIONAL N.V.: KEY STRATEGIC MOVES AND DEVELOPMENTS

TABLE 106. TOYOTA MOTOR CORPORATION: COMPANY SNAPSHOT

TABLE 107. TOYOTA MOTOR CORPORATION: OPERATING SEGMENTS

TABLE 108. TOYOTA MOTOR CORPORATION: PRODUCT PORTFOLIO

TABLE 109. TOYOTA MOTOR CORPORATION: KEY STRATEGIC MOVES AND DEVELOPMENTS LIST OF FIGURES

FIGURE 01. KEY MARKET SEGMENTS

FIGURE 02. EXECUTIVE SUMMARY

FIGURE 03. EXECUTIVE SUMMARY

FIGURE 04. TOP IMPACTING FACTORS

FIGURE 05. TOP INVESTMENT POCKETS

FIGURE 06. TOP WINNING STRATEGIES, BY YEAR, 2017-2020*

FIGURE 07. TOP WINNING STRATEGIES, BY DEVELOPMENT, 2017-2020*

FIGURE 08. TOP WINNING STRATEGIES, BY COMPANY, 2017-2020*

FIGURE 09. MARKET SHARE ANALYSIS, 2019 (%)

FIGURE 10. GLOBAL SMART MOBILITY MARKET, BY ELEMENT, 2019-2027

FIGURE 11. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET FOR BIKE COMMUTING, BY COUNTRY, 2019 & 2027 ($MILLON)

FIGURE 12. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET FOR CAR SHARING, BY COUNTRY, 2019 & 2027 ($MILLON)

FIGURE 13. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET FOR RIDESHARING, BY COUNTRY, 2019 & 2027 ($MILLON)

FIGURE 14. GLOBAL SMART MOBILITY MARKET, BY SOLUTION, 2019-2027

FIGURE 15. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET FOR TRAFFIC MANAGEMENT, BY COUNTRY, 2019 & 2027 ($MILLON)

FIGURE 16. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET FOR PARKING MANAGEMENT, BY COUNTRY, 2019 & 2027 ($MILLON)

FIGURE 17. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET FOR MOBILITY MANAGEMENT, BY COUNTRY, 2019 & 2027 ($MILLON)

FIGURE 18. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET FOR OTHERS, BY COUNTRY, 2019 & 2027 ($MILLON)

FIGURE 19. GLOBAL SMART MOBILITY MARKET, BY TECHNOLOGY, 2019-2027

FIGURE 20. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET FOR 3G & 4G, BY COUNTRY, 2019 & 2027 ($MILLON)

FIGURE 21. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET FOR WI-FI, BY COUNTRY, 2019 & 2027 ($MILLON)

FIGURE 22. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET FOR GNSS/GPS, BY COUNTRY, 2019 & 2027 ($MILLON)

FIGURE 23. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET FOR RFID, BY COUNTRY, 2019 & 2027 ($MILLON)

FIGURE 24. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET FOR EMBEDDED SYSTEMS, BY COUNTRY, 2019 & 2027 ($MILLON)

FIGURE 25. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET FOR OTHERS, BY COUNTRY, 2019 & 2027 ($MILLON)

FIGURE 26. SMART MOBILITY MARKET, BY REGION, 2019-2027 (%)

FIGURE 27. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET, BY COUNTRY, 2019–2027 (%)

FIGURE 28. U.S. SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 29. CANADA SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 30. MEXICO SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 31. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET, BY COUNTRY, 2019–2027 (%)

FIGURE 32. GERMANY SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 33. FRANCE SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 34. UK SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 35. ITALY SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 36. REST OF EUROPE SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 37. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET, BY COUNTRY, 2019–2027 (%)

FIGURE 38. CHINA SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 39. JAPAN SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 40. INDIA SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 41. SOUTH KOREA SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 42. REST OF ASIA-PACIFIC SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 43. COMPARATIVE SHARE ANALYSIS OF SMART MOBILITY MARKET, BY COUNTRY, 2019–2027 (%)

FIGURE 44. LATIN AMERICA SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 45. MIDDLE EAST SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 46. AFRICA SMART MOBILITY MARKET, 2019–2027 ($MILLION)

FIGURE 47. CISCO: NET SALES, 2017–2019 ($MILLION)

FIGURE 48. CISCO: REVENUE SHARE BY SEGMENT, 2019 (%)

FIGURE 49. CISCO: REVENUE SHARE BY REGION, 2019 (%)

FIGURE 50. FORD MOTOR COMPANY: NET SALES, 2017–2019 ($MILLION)

FIGURE 51. FORD MOTOR COMPANY: REVENUE SHARE BY SEGMENT, 2019 (%)

FIGURE 52. FORD MOTOR COMPANY: REVENUE SHARE BY REGION, 2019 (%)

FIGURE 53. ROBERT BOSCH GMBH: NET SALES, 2017–2019 ($MILLION)

FIGURE 54. ROBERT BOSCH GMBH: REVENUE SHARE BY SEGMENT, 2019 (%)

FIGURE 55. ROBERT BOSCH GMBH: REVENUE SHARE BY REGION, 2019 (%)

FIGURE 56. SIEMENS: REVENUE, 2017–2019 ($MILLION)

FIGURE 57. SIEMENS: REVENUE SHARE BY SEGMENT, 2019 (%)

FIGURE 58. SIEMENS: REVENUE SHARE BY REGION, 2019 (%)

FIGURE 59. TOMTOM INTERNATIONAL N.V.: NET SALES, 2017–2019 ($MILLION)

FIGURE 60. TOMTOM INTERNATIONAL N.V.: REVENUE SHARE BY SEGMENT, 2019 (%)

FIGURE 61. TOMTOM INTERNATIONAL N.V.: REVENUE SHARE BY REGION, 2019 (%)

FIGURE 62. TOYOTA MOTOR CORPORATION: NET SALES, 2017–2019 ($MILLION)

FIGURE 63. TOYOTA MOTOR CORPORATION: REVENUE SHARE BY SEGMENT, 2019 (%)

FIGURE 64. TOYOTA MOTOR CORPORATION: REVENUE SHARE BY REGION, 2019 (%)