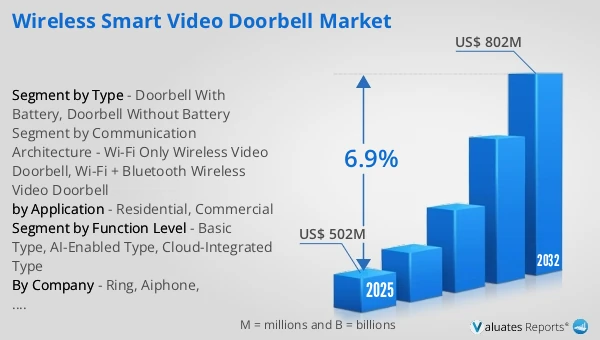

The global Wireless Smart Video Doorbell market was valued at US$ 502 million in 2025 and is anticipated to reach US$ 802 million by 2032, at a CAGR of 6.9% from 2026 to 2032.

Wireless Smart Video Doorbell Market

The 2025 U.S. tariff policies introduce profound uncertainty into the global economic landscape. This report critically examines the implications of recent tariff adjustments and international strategic countermeasures on Wireless Smart Video Doorbell competitive dynamics, regional economic interdependencies, and supply chain reconfigurations.

A wireless smart video doorbell is a front-door smart security and communication endpoint built around wireless connectivity (most commonly Wi-Fi, often with Bluetooth-assisted onboarding and in some cases alternative wireless backhaul), integrating a camera, illumination, microphone, and speaker to enable live viewing, two-way talk, event alerts, and recorded evidence when occupants are at home or away. It addresses the core limitations of traditional doorbells—no visual verification, limited remote response, and weak traceability of doorstep incidents—while supporting high-frequency doorstep scenarios such as deliveries, ad-hoc visitors, and remote caregiving. Historically, the category can be traced to two converging product lineages: wired video intercom door stations used in multi-dwelling buildings and home security cameras focused on remote monitoring and recording. As home broadband, smartphones, and push-notification ecosystems matured, “wireless + app” doorbells emerged as consumer-friendly, self-installed products; subsequent advances in low-power imaging, wireless modules, cloud services, and edge computing further shifted the device into an “entryway node” that orchestrates workflows with smart locks, indoor chimes, home hubs, and broader smart-home platforms. Upstream inputs typically include enclosure and protection materials (engineering plastics or metal housings, glass/acrylic covers, gaskets and waterproof adhesives, thermal interface materials and protective coatings) and key electronic/optical components and modules (CMOS image sensors, lens assemblies and IR filters, IR LEDs and drivers, microphones and speakers, audio codecs/amplifiers, SoC/MCU processors, memory, Wi-Fi/Bluetooth RF parts and antennas, power management and charging ICs, batteries with protection/gauging, passives and connectors), plus installation accessories (buttons/triggers, mounting brackets/fasteners, and optional indoor chimes/repeaters). These materials and components are typically sourced from established consumer electronics, security camera, and IoT wireless connectivity supply chains, and then integrated by OEMs through RF tuning, power optimization, weatherproof reliability validation, and firmware–app–cloud integration for mass production.In 2025, the global production capacity of wireless smart video doorbells was 10 million units, with sales reaching 8.01 million units. The average selling price was USD 62.7 per unit, and industry gross margins generally ranged between 30% and 40%.

The market is shifting from a “single-device bestseller” mindset to system-level competition around the entryway as a strategic node. On the consumer side, wireless smart video doorbells are increasingly positioned as the front-end of home security and smart-home workflows, where differentiation depends less on raw image quality and more on end-to-end reliability: timely notifications, controllable false alerts, acceptable talk latency, consistent performance under weak networks, and seamless linkage with smart locks, indoor chimes, and home hubs. E-commerce remains the dominant channel, but bundling with broadband/telecom partners, smart-home platforms, and new-home packages is growing, reinforcing a device-plus-service model. On the supply side, mature ODM ecosystems and modular components have accelerated hardware commoditization, shifting real differentiation to app UX, detection logic, cloud/service reliability, privacy posture, and after-sales execution; demand is also rising in light-managed scenarios such as rentals and small multi-occupant properties, where permissions, visitor logs, and remote management matter more.

Future evolution will follow three main paths: stronger edge intelligence, more engineered connectivity and power performance, and deeper platform/compliance capabilities. Edge AI will prioritize on-device event filtering and key recognition, turning false-alert governance into a core battleground and expanding from basic detection to richer doorstep-context understanding that makes alerts more actionable and automations more controlled. Multi-signal fusion (video plus audio and optional sensing) will be increasingly used to maintain robustness in challenging conditions such as low light, glare, rain/fog, and partial occlusion. On the connectivity and power front, battery experience will be optimized more systematically through finer wake strategies, edge buffering, coordination with indoor repeaters/hubs, and RF adaptation to difficult building environments—reducing the “works on paper but feels unstable” gap. Platform-wise, tighter integration with smart locks and security platforms will bring unified identity/permission models, cross-device rules, and more operational tooling such as health monitoring and remote provisioning; at the same time, rising privacy and cybersecurity expectations will push vendors toward standardized encryption, data minimization, access governance, auditability, and lifecycle controls.

Growth drivers include the continued rise in doorstep events and stronger security expectations—deliveries, ad-hoc visitors, remote caregiving, and community needs for traceable incident records all increase willingness to adopt. The spread of smart locks and whole-home automation further elevates the doorbell into a natural trigger point for coordinated workflows and ecosystem consistency. Constraints remain significant, especially around experience volatility and compliance cost: wireless interference, router distance, and door materials can cause dropouts and latency; outdoor durability, weatherproofing, anti-tamper design, and cold-temperature operation increase manufacturing and quality-consistency challenges; fragmented ecosystems limit cross-brand interoperability; and cloud dependence introduces subscription fatigue as well as data governance and privacy compliance burdens. Under intense price pressure and hardware commoditization, vendors must continuously balance on-device compute with battery life, cloud investment with user value, and hardware pricing with service commitments—pushing the market toward stratification led by stable performance, strong privacy/security readiness, and sustainable service capability.

This report delivers a comprehensive overview of the global Wireless Smart Video Doorbell market, with both quantitative and qualitative analyses, to help readers develop growth strategies, assess the competitive landscape, evaluate their position in the current market, and make informed business decisions regarding Wireless Smart Video Doorbell. The Wireless Smart Video Doorbell market size, estimates, and forecasts are provided in terms of sales volume (K Units) and revenue (US$ millions), with 2025 as the base year and historical and forecast data for 2021–2032.

The report segments the global Wireless Smart Video Doorbell market comprehensively. Regional market sizes by Type, by Application, by Communication Architecture, and by company are also provided. For deeper insight, the report profiles the competitive landscape, key competitors, and their respective market rankings, and discusses technological trends and new product developments.

This report will assist Wireless Smart Video Doorbell manufacturers, new entrants, and companies across the industry value chain with information on revenues, sales volume, and average prices for the overall market and its sub-segments, by company, by Type, by Application, and by region.

Market Segmentation

Scope of Wireless Smart Video Doorbell Market Report

| Report Metric |

Details |

| Report Name |

Wireless Smart Video Doorbell Market |

| Accounted market size in 2025 |

US$ 502 million |

| Forecasted market size in 2032 |

US$ 802 million |

| CAGR |

6.9% |

| Base Year |

2025 |

| Forecasted years |

2026 - 2032 |

| Segment by Type |

- Doorbell With Battery

- Doorbell Without Battery

|

| Segment by Communication Architecture |

- Wi-Fi Only Wireless Video Doorbell

- Wi-Fi + Bluetooth Wireless Video Doorbell

|

| Segment by Function Level |

- Basic Type

- AI-Enabled Type

- Cloud-Integrated Type

|

| by Application |

|

| Consumption by Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia)

- Asia-Pacific (China, Japan, South Korea, Taiwan)

- Southeast Asia (India)

- Latin America (Mexico, Brazil)

|

| By Company |

Ring, Aiphone, Panasonic, August, Skybell, Honeywell, Legrand, Commax, Advente, Kivos, Jiale, Dnake, RL, Genway, Anjubao, Leelen, Aurine, Samsung, TCS, ABB, Guangdong Roule Electronics, Hager, Fermax |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |

Chapter Outline

- Chapter 1: Defines the scope of the report and presents an executive summary of market segments (by Type, by Application, by Communication Architecture, etc.), including the size of each segment and its future growth potential. It offers a high-level view of the current market and its likely evolution in the short, medium, and long term.

- Chapter 2: Provides a detailed analysis of the competitive landscape for Wireless Smart Video Doorbell manufacturers, covering pricing, sales and revenue shares, latest development plans, and mergers and acquisitions.

- Chapter 3: Examines Wireless Smart Video Doorbell sales and revenue at the regional and country levels. It quantifies market size and growth potential for each region and its key countries, and outlines market development, outlook, addressable space, and national market size.

- Chapter 4: Analyzes segments by Type, detailing the size and growth potential of each segment to help readers identify “blue ocean” opportunities.

- Chapter 5: Analyzes market segments by Application, covering the size and growth potential of each segment to help readers identify “blue ocean” opportunities in downstream markets.

- Chapter 6: Profiles key players, presenting core information on leading companies, including product sales, revenue, pricing, gross margin, product portfolio/introductions, and recent developments.

- Chapter 7: Reviews the industry value chain, including upstream and downstream segments.

- Chapter 8: Discusses market dynamics and recent developments, including drivers, restraints, challenges and risks for manufacturers, U.S. Tariffs and relevant policy analysis.

- Chapter 9: Summarizes the key findings and conclusions of the report.

Ans: The main players in the Wireless Smart Video Doorbell Market are Ring, Aiphone, Panasonic, August, Skybell, Honeywell, Legrand, Commax, Advente, Kivos, Jiale, Dnake, RL, Genway, Anjubao, Leelen, Aurine, Samsung, TCS, ABB, Guangdong Roule Electronics, Hager, Fermax