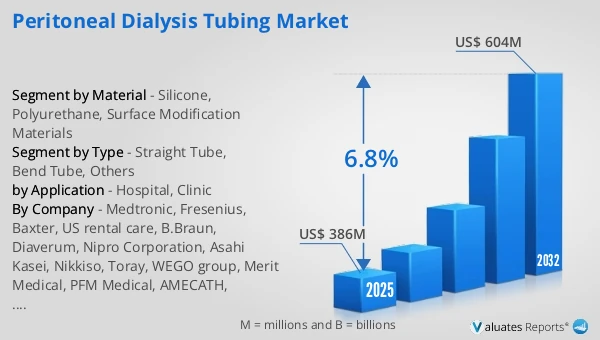

The global Peritoneal Dialysis Tubing market was valued at US$ 386 million in 2025 and is anticipated to reach US$ 604 million by 2032, at a CAGR of 6.8% from 2026 to 2032.

Peritoneal Dialysis Tubing Market

The 2025 U.S. tariff policies introduce profound uncertainty into the global economic landscape. This report critically examines the implications of recent tariff adjustments and international strategic countermeasures on Peritoneal Dialysis Tubing competitive dynamics, regional economic interdependencies, and supply chain reconfigurations.

Peritoneal Dialysis Tubing generally refers to medical tubing assemblies that safely transfer dialysate between solution bags/warming devices/cycler systems and the patient’s peritoneal access pathway. This includes extension and connection lines used with transfer sets in CAPD, as well as disposable tubing sets designed to interface with automated peritoneal dialysis (APD) cyclers. The core problem it solves is delivering a low-leakage, low-contamination-exposure, and low-use-error fluid pathway under repeated fill-and-drain cycles and frequent connect/disconnect events—often in home settings where user technique can vary—while maintaining stable flow, reliable connections, and design-mediated barriers against microbial ingress, backflow contamination, occlusion, and kink-related access failure. Its evolution mirrors the development of PD therapy models: early PD relied on simpler tubing connections with less consistent infection control, but as CAPD expanded, Y-set and double-bag systems emphasizing reduced touch and reduced open exposure became mainstream, driving tubing from “simple lines” toward more integrated assemblies with clamps, branches, and (depending on design) filtration or valve/check functions. With the growth of APD, tubing sets further converged with cycler interface standards, pumping rhythms, and pressure/flow management requirements, increasing emphasis on assembly precision, fatigue resistance, and batch-to-batch consistency to support stable overnight automated therapy. Upstream materials and components typically include medical-grade thermoplastics and elastomers (e.g., PVC, TPU, TPE, silicone) for extruded tubing with requirements for clarity, flexibility, and kink resistance; precision injection-molded connectors and manifolds (often PP, PC, ABS, or medical copolymers depending on chemical resistance and strength needs); clamps and flow-control elements to reduce misuse; optional filters, drip chambers, and check/valve structures depending on configuration; bonding/welding and sealing materials aligned to solvent bonding, heat sealing, or ultrasonic welding processes; and sterile barrier packaging and sterilization-related materials (medical papers, Tyvek, blister trays, pouches, indicators, and labels). The upstream supply chain is commonly formed by medical resin and compound suppliers, extrusion and tubing-assembly processors, precision molding/tooling specialists, sealing/valve component vendors, sterile packaging suppliers, and sterilization service providers, with final cleanroom assembly, leak/flow consistency testing, packaging qualification, and sterilization release handled by PD consumables manufacturers.In 2025, the global production capacity of peritoneal dialysis catheters reached 7.0 million units, with sales volume totaling 5.127 million units. The average selling price was approximately USD 75.3 per unit, and manufacturers’ gross margins were generally in the range of 20% to 30%.

The PD tubing market is currently defined by strong platform lock-in, high quality thresholds, and a heavy dependence on supply-chain stability to protect clinical confidence. In both CAPD and APD pathways, tubing is tightly coupled with specific connection systems, transfer sets, or cycler interfaces, so providers and patients often prefer to stay within an established platform to minimize adverse-event risk and training burden. As a result, competition is less about “tubing as a commodity” and more about ecosystem performance across the full access workflow. Clinicians focus on sterile connection reliability, seal integrity and fatigue resistance under repeated use, clarity of flow-control elements (clamps/branches/misuse-proofing), and robust lot-to-lot consistency with traceability. Even small process variations can translate into leakage, occlusion, breakage, or contamination exposure, amplifying infection-control concerns and liability pressure. This pushes suppliers to invest in clean manufacturing, precise assembly, rigorous leak testing, and validated packaging/sterilization. Leading players reinforce stickiness through long-term validation, interface standards, and training infrastructure, while regional entrants must first overcome compatibility validation, quality-system maturity, and stable supply capability.

Future development will center on lowering contamination exposure, reducing use errors, improving home usability, and expanding digital management—while differentiating along CAPD versus APD needs. For CAPD, tubing assemblies will continue evolving toward more closed, reduced-touch/reduced-exposure connection concepts, with stronger port protection, clearer connection feedback, and (depending on platform design) backflow prevention or misconnection mitigation to lower the learning curve for new patients. For APD, the emphasis will remain on highly reliable cycler interfaces, stable fluid-path performance, and enhanced cyclic fatigue resistance aligned with more complex overnight therapy rhythms, alongside ongoing improvements in assembly consistency and ease of setup. In parallel, consumable management will shift from compliance-only traceability to operational optimization: UDI/barcode integration with hospital supply systems or home-delivery networks can enable tighter lot control, faster recall response, and closed-loop patient education. In some markets, vendors will increasingly bundle remote training, usage guidance, and follow-up support into broader solution offerings, positioning tubing not just as a consumable but as a pathway-quality enabler.

Key drivers include healthcare systems’ sustained push to expand home dialysis, improve resource efficiency, and enhance patient experience. Nursing constraints and workflow pressure favor standardized, easier-to-train tubing platforms, accelerating adoption where providers can demonstrate safer routines and fewer failures. Guideline and quality-metric attention to peritonitis, access dysfunction, and readmissions further elevates the connection/tubing step as a high-leverage control point. Major constraints include switching resistance created by platform lock-in, compliance-driven change costs, and supply volatility. Once a pathway becomes entrenched, platform switching typically requires substantial training and convincing real-world evidence. Meanwhile, any adjustment to tubing materials, bonding/welding processes, sterilization methods, or packaging structures can trigger revalidation and regulatory change-control burden, slowing iteration. Finally, fluctuations in key resins and additives, precision molded components, and sterilization/sterile packaging capacity can disrupt deliveries and undermine confidence—becoming a practical barrier to rapid scaling, especially for newer entrants.

This report delivers a comprehensive overview of the global Peritoneal Dialysis Tubing market, with both quantitative and qualitative analyses, to help readers develop growth strategies, assess the competitive landscape, evaluate their position in the current market, and make informed business decisions regarding Peritoneal Dialysis Tubing. The Peritoneal Dialysis Tubing market size, estimates, and forecasts are provided in terms of sales volume (K Units) and revenue (US$ millions), with 2025 as the base year and historical and forecast data for 2021–2032.

The report segments the global Peritoneal Dialysis Tubing market comprehensively. Regional market sizes by Type, by Application, by Material, and by company are also provided. For deeper insight, the report profiles the competitive landscape, key competitors, and their respective market rankings, and discusses technological trends and new product developments.

This report will assist Peritoneal Dialysis Tubing manufacturers, new entrants, and companies across the industry value chain with information on revenues, sales volume, and average prices for the overall market and its sub-segments, by company, by Type, by Application, and by region.

Market Segmentation

Scope of Peritoneal Dialysis Tubing Market Report

| Report Metric |

Details |

| Report Name |

Peritoneal Dialysis Tubing Market |

| Accounted market size in 2025 |

US$ 386 million |

| Forecasted market size in 2032 |

US$ 604 million |

| CAGR |

6.8% |

| Base Year |

2025 |

| Forecasted years |

2026 - 2032 |

| Segment by Type |

- Straight Tube

- Bend Tube

- Others

|

| Segment by Material |

- Silicone

- Polyurethane

- Surface Modification Materials

|

| by Application |

|

| Consumption by Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia)

- Asia-Pacific (China, Japan, South Korea, Taiwan)

- Southeast Asia (India)

- Latin America (Mexico, Brazil)

|

| By Company |

Medtronic, Fresenius, Baxter, US rental care, B.Braun, Diaverum, Nipro Corporation, Asahi Kasei, Nikkiso, Toray, WEGO group, Merit Medical, PFM Medical, AMECATH, AdvinHealthcare |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |

Chapter Outline

- Chapter 1: Defines the scope of the report and presents an executive summary of market segments (by Type, by Application, by Material, etc.), including the size of each segment and its future growth potential. It offers a high-level view of the current market and its likely evolution in the short, medium, and long term.

- Chapter 2: Provides a detailed analysis of the competitive landscape for Peritoneal Dialysis Tubing manufacturers, covering pricing, sales and revenue shares, latest development plans, and mergers and acquisitions.

- Chapter 3: Examines Peritoneal Dialysis Tubing sales and revenue at the regional and country levels. It quantifies market size and growth potential for each region and its key countries, and outlines market development, outlook, addressable space, and national market size.

- Chapter 4: Analyzes segments by Type, detailing the size and growth potential of each segment to help readers identify “blue ocean” opportunities.

- Chapter 5: Analyzes market segments by Application, covering the size and growth potential of each segment to help readers identify “blue ocean” opportunities in downstream markets.

- Chapter 6: Profiles key players, presenting core information on leading companies, including product sales, revenue, pricing, gross margin, product portfolio/introductions, and recent developments.

- Chapter 7: Reviews the industry value chain, including upstream and downstream segments.

- Chapter 8: Discusses market dynamics and recent developments, including drivers, restraints, challenges and risks for manufacturers, U.S. Tariffs and relevant policy analysis.

- Chapter 9: Summarizes the key findings and conclusions of the report.

Ans: The main players in the Peritoneal Dialysis Tubing Market are Medtronic, Fresenius, Baxter, US rental care, B.Braun, Diaverum, Nipro Corporation, Asahi Kasei, Nikkiso, Toray, WEGO group, Merit Medical, PFM Medical, AMECATH, AdvinHealthcare